Is Your HDB Building Wealth

Or Quietly Becoming a Retirement Risk?

Take the Free Singapore HDB Asset Performance Scorecard

To Find Out

Your HDB Is Probably Your Largest Asset

You Could Be Sitting on a $900,000 HDB… and Still Fall Short in Retirement.

Imagine Retiring at 65…

You own a fully paid HDB worth $900,000.

You think you’re financially secure.

Then you discover:

- Most of the proceeds are tied up in CPF refunds.

- Your cash proceeds are much lower than expected.

- Your retirement income still falls short.

That’s why I created the HDB Asset Performance Scorecard.

Many Singapore homeowners assume their flat will fund their retirement.

But with rising living costs, CPF requirements, and lease decay, holding your HDB without a strategy may quietly reduce your retirement potential.

I help HDB owners analyse, optimise and restructure their property assets so their home becomes a retirement advantage — not a liability.

TAKE THE SINGAPORE HDB ASSET PERFORMANCE SCORECARD

This simple 5-minute assessment evaluates your property across key factors:

✔ Lease risk exposure

✔ CPF capital lock-in

✔ Growth efficiency

✔ Retirement runway

✔ Strategic flexibility

At the end, you will receive a clear rating:

🟢 Performing Asset

🟡 Underperforming Asset

🔴 Retirement Risk Exposure

Your HDB is likely your largest financial asset.

It deserves more than guesswork.

This Scorecard Is Perfect If…

✅ Your HDB is over 10–15 years old

✅ You think your HDB has made good money

✅ You’re wondering if you should hold or upgrade

✅ You’re planning for retirement

✅ You don’t know how much cash you’ll actually receive after selling

Take the Singapore HDB Asset Performance Scorecard today and find out whether your property is helping or hurting your retirement strategy.

Takes 5 minutes. You’ll get your rating instantly, plus a personalised breakdown call if you want one.

Some homeowners discover the best decision is to hold their current HDB. My recommendations are based on your numbers—not on making a transaction.

THE RETIREMENT REALITY IN SINGAPORE

Most Singaporeans rely on three pillars for retirement:

• CPF savings

• Property wealth

• Personal investments

But the reality is that CPF retirement requirements continue to rise to keep pace with inflation.

For example, the Full Retirement Sum set by the Central Provident Fund Board increases regularly to reflect rising living costs.

At the same time, housing policies governed by the Housing & Development Board ensure housing stability — but they also mean property growth is not unlimited.

This creates an important question:

Is your HDB property actually helping you build retirement wealth — or just holding your capital?

Most homeowners have never analysed this properly.

Are You Underprepared for Retirement?

1. Understand What CPF Actually Covers

CPF was never designed to fund a comfortable retirement.

It was designed to fund basic living.

As reported, CPF LIFE payouts are meant to cover households in the lower-middle expenditure tier, not a middle-class lifestyle

Here’s what CPF provides today (Age 65 payouts):

| Retirement Tier | Amount at 55 (2026 est.) | Monthly CPF LIFE payout |

| BRS (Basic Retirement Sum) | $110K | $770 – $830 |

| FRS (Full Retirement Sum) | $220K | $1,540 – $1,660 |

| ERS (Enhanced Retirement Sum) | $440K | $3,180 – $3,410 |

So… Even max CPF (ERS) gives about $3.2K/month per person

2. Real Retiree Spending in Singapore

Studies show retirees spend approximately:

| Housing Type | Ave Monthly Spend per Person |

| HDB 3-room | est. $1,100 |

| HDB 4-room | est. $1,200 |

| HDB 5-room | est. $1,500 |

That’s basic lifestyle only.

No travel.

No lifestyle upgrades.

No private healthcare buffer.

So… for a couple: Basic living = $2,400 – $3,000/month

3. What is a “Comfortable” Retirement (Couple)?

A comfortable Singapore retirement typically includes:

- Dining flexibility

- Travel (1-2 trips/year)

- Medical buffer

- insurance premiums

- Transport

- Gifting/family support

- Lifestyle inflation

Realistic comfortable monthly breakdown

| Category | Monthly |

|---|---|

| Food & groceries | $1,200 |

| Utilities & bills | $250 |

| Transport | $300 |

| Insurance | $400 |

| Mobile/Internet | $150 |

| Healthcare buffer | $800 |

| Lifestyle & dining | $1,300 |

| Travel fund | $500 |

| Contingency buffer | $600 |

| Total | $5,500/month |

4. The Retirement Gap

| Monthly/25 Years | Comfortable need | Typical CPF (FRS Couple) | Gap |

|---|---|---|---|

| Monthly | $5,500/month | $3,200/month | $2,300/month |

| Over 25 Years | $1,650,000 | $960,000 | $690,000 |

That gap must come from:

- Property

- Investments

- Cash flow assets

How most Singaporeans fall into the HDB Retirement Trap

Is your HDB property actually helping you build retirement wealth – or just holding your capital?

For most Singaporeans:

👉 Property = largest asset

But the problem:

❌ No income generated

❌ Wealth is “locked”

Most HDB Owners Believe Their Flat Will Find Retirement

But here’s the uncomfortable truth:

Between:

- CPF accrued interest

- Mortgage interest

- Lease decay

- Stagnant resale growth

Many homeowners are unknowingly shrinking their retirement capital.

Regulations governed by the Housing & Development Board protect housing affordability — but they also limit capital upside in certain scenarios.

Why Many HDB Owners Get Stuck

Many property decisions are made emotionally:

• “My neighbour sold for $800k.”

• “The market is hot now.”

• “Let’s just hold longer.”

But strategic property planning should answer deeper questions:

• How much cash will you actually receive after CPF refund?

• Is your equity compounding efficiently?

• When does lease decay start affecting buyer demand?

• Should you restructure before retirement?

Without proper planning, some homeowners only realise the limitations when it is too late to optimise their asset.

Introducing

The HDB Asset Performance Scorecard

This scorecard will help you determine:

✔ Is your HDB compounding wealth?

✔ Or is it slowly becoming a retirement liability?

✔ Should you hold, restructure, or upgrade?

A simple but powerful assessment to determine whether your HDB is:

🟢 Performing

🟡 Underperforming

🔴 At Risk of Becoming a Retirement Trap

In just 5 minutes, you will evaluate:

✔ Lease risk exposure

✔ CPF capital lock-in

✔ Growth efficiency

✔ Retirement runway

✔ Strategic flexibility

This is not a valuation.

This is a capital performance check.

ABOUT STEVEN CHIA

Steven Chia (CEA No: R029037A) has been in the Singapore property market since 2008.

Over the years, he has helped more than one hundred homeowners navigate complex property decisions involving HDB regulations, CPF implications and market cycles.

His focus today is helping homeowners view property not just as housing — but as a strategic asset within their retirement planning.

WHY I AM DIFFERENT FROM MOST PROPERTY AGENTS

Most agents focus on transactions.

I focus on asset performance.

Instead of asking you, “Do you want to sell?”

I ask, “Is your property working hard enough for your retirement?”

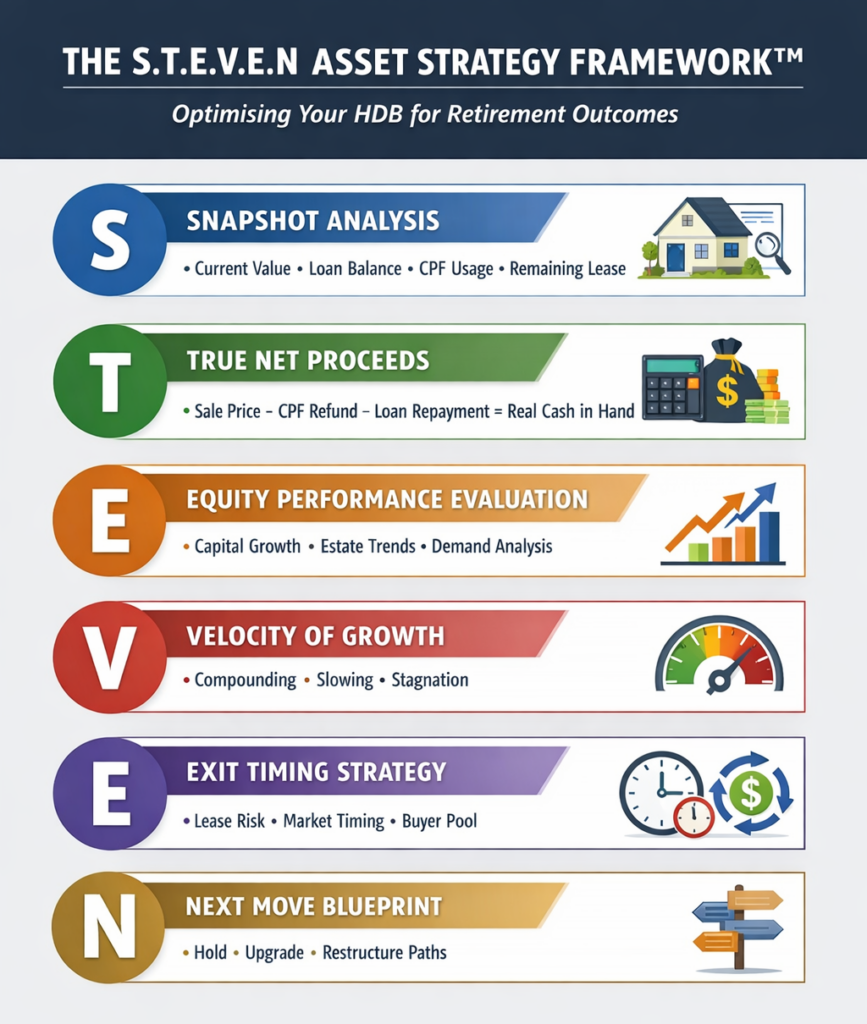

INTRODUCING

THE S.T.E.V.E.N STRATEGY FRAMEWORK

After helping homeowners navigate property decisions since 2008, I developed a structured methodology to analyse property performance.

This framework helps clients understand whether their property is optimised for retirement outcomes.

S – Snapshot Analysis

We review your full asset position.

• Current property value

• Outstanding loan

• CPF usage and accrued interest

• Remaining lease

This gives a clear starting point.

T – True Net Proceeds

Most people look at the selling price.

But the real question is:

How much cash will you actually keep?

We calculate:

• CPF refund obligations

• Loan redemption

• Estimated fees

• Net liquidity

E – Equity Performance Evaluation

Your property should behave like an asset.

We evaluate:

• Growth trends

• Estate development cycle

• Demand sustainability

V – Velocity of Growth

We analyse how your capital is growing.

Is your property:

• Compounding

• Slowing

• Or stagnating?

This helps determine whether holding longer makes sense.

E – Exit Timing Strategy

Timing matters.

We assess:

• Lease sensitivity

• Market demand cycle

• Buyer financing limitations

N – Next Move Blueprint

Finally, we map possible strategies:

• Hold and optimise

• Upgrade strategically

• Restructure ownership

• Redeploy capital

This ensures your property decision supports your long-term retirement plan.

Before Making Your Next Property Decision

Ask yourself:

• Do you know how much CPF must be refunded if you sell?

• Do you know your true cash proceeds?

• Do you know if your property is still compounding wealth?

• Do you know when lease decay becomes a real factor?

If you cannot answer these questions clearly, you may be making one of the biggest financial decisions without enough information.